Not long ago, accessing a Bridgewater Associates portfolio required a nine-figure institutional relationship, a legal team, and years of patience.

Today it requires a brokerage account and knowing what ticker symbol to type in the search bar.

The ETF wrapper has become the most powerful distribution mechanism in the history of asset management, and the industry is now using it to move strategies that were built for endowments and sovereign wealth funds into the hands of everyday advisors and their clients.

What is happening right now is bigger than a product cycle.

The pace of institutional strategy adoption into the ETF wrapper has become difficult to ignore, and the question of what belongs inside it is being rewritten in real time.

What “Institutional Only” Actually Meant

The walls that kept these strategies exclusive were built on genuine structural realities.

Structured notes carried upfront commissions as high as 5%, locked capital until maturity, and exposed buyers directly to the issuing bank’s credit risk. Hedge fund access sat behind accreditation requirements, multi-year lock-up periods, and K-1 tax statements. Private credit demanded illiquidity tolerance that most mandates simply could not accommodate.

These were products designed for investors who could afford to wait, absorb complexity, and hire professionals to manage the paperwork. For decades, that thesis held up.

Then the ETF wrapper changed it.

Strategies That Have Crossed Over

The list of strategies that crossed into the ETF wrapper in the past 12 months reads like an alternatives catalog from five years ago.

Autocallable structured notes. Hedge fund risk parity. True long and short global equity. Private credit. Money market funds. Derivative income structures.

The velocity is what stands out. Nearly 1,000 active ETFs launched in 2025, sharply higher than the 584 introduced the year before, with alternative and short-term strategies alone accounting for more than 340 of those launches. Since 2022, nearly 2,000 non-traditional ETPs have come to market, accounting for roughly 70% of new ETF/ETP introductions and attracting nearly $227 billion in inflows in 2025 alone. The wrapper has become the destination of choice for product innovation at every level of the complexity spectrum.

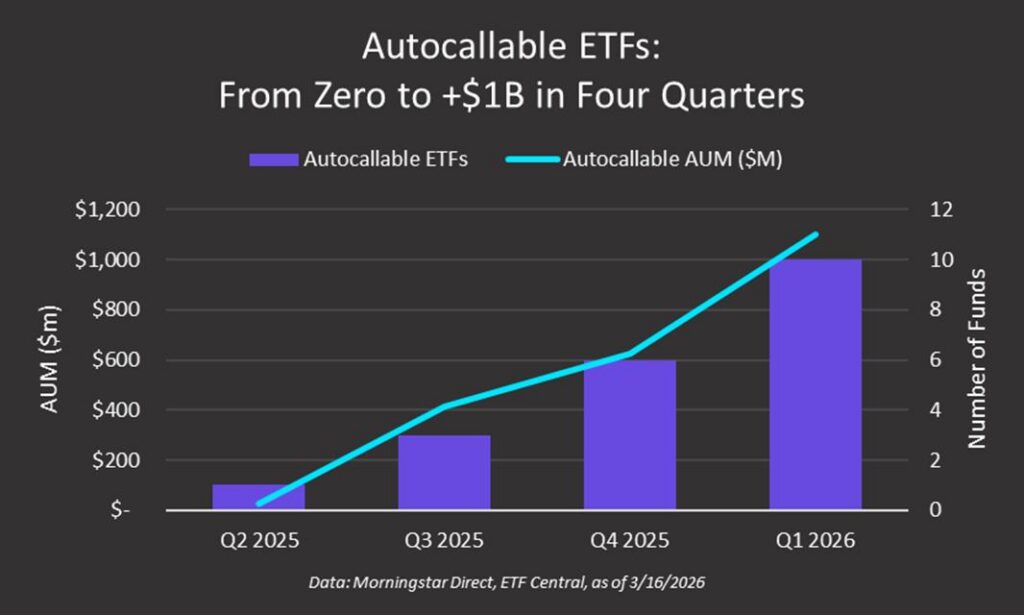

Consider the autocallable market. In 2024 alone, autocallable structured notes accounted for over $104 billion in issuance, representing more than two thirds of the entire structured products market. That market existed almost entirely behind closed doors, accessible through private placements with significant minimums and no secondary market to speak of.

The first autocallable ETF launched in June 2025, and by late December it had crossed $500 million in AUM in roughly six months. Multiple issuers followed within months. The broader derivative income ETF universe has grown 255% since the beginning of 2023 and now sits at ~$120 billion in assets.

The hedge fund side of the ledger moved just as quickly.

Bridgewater’s All-Weather strategy had been held exclusively by large institutions and ultra-high-net-worth investors since its inception in 1996. That 30-year-old institutional framework is now a single-ticker ETF, gathering $600+ million in its first year on market.

Long and short global equity strategies, the structural foundation of traditional hedge fund management, have also arrived in ETF wrapper form, with funds offering genuine short exposure across international markets at institutional-level turnover.

Private credit represents perhaps the most structurally complicated crossing.

The private credit market stands at roughly $3 trillion, a sector that was almost entirely exclusive to institutional players and high-net-worth individuals until 2025. The first private credit ETF launched in early 2025, engineered around a liquidity backstop arrangement on the private sleeve to make daily redemptions workable. The fund has outperformed 92% of its Morningstar category peers, even as flows have been modest while advisors evaluate the structural mechanics.

For institutional allocators and advisors who have worked with these strategies in their original form, the wrapper brings familiar risk and return profiles into a more operationally efficient, tax-advantaged, and liquid vehicle. The structural trade-offs are real and worth understanding, but the strategies themselves are not new to this audience.

What Made This Possible

Three forces converged to produce this moment.

The in-kind creation and redemption mechanism solved the tax problem that made many of these strategies unattractive in a fund structure, allowing issuers to bring complex instruments into the ETF wrapper without triggering the capital gains consequences that would have made them a hard sell. A more tolerant regulatory environment at the SEC cleared the path for structures that had been waiting in the queue for years. And intense issuer competition pushed product development well beyond vanilla equity and fixed income into territory that would have seemed unlikely just a few years ago.

Each of these conditions existed independently for some time. Their convergence is what turned possibility into a filing frenzy.

Honest Caveat

Access and comprehension are not the same thing, and the ETF industry would do well to hold that distinction carefully.

Autocallable structures carry coupon barriers, early redemption triggers, and real principal risk in severe drawdowns. Long and short equity funds can generate meaningful volatility and tax complexity that surprises advisors accustomed to the cleaner profile of passive ETFs. Private credit ETFs are still working through fundamental questions about how daily liquidity interacts with underlying asset illiquidity at scale.

Product innovation has moved faster than the educational infrastructure around it, and advisors sitting across from clients who bought these products carry the weight of that.

The View from the Platform

Tidal operates infrastructure for funds across the complexity spectrum, and the shift is visible in real time.

The strategies asset managers are bringing to market today look fundamentally different from what was being built three years ago. The operational demands are higher, the capital markets considerations are more layered, and the education requirements have grown alongside the complexity of the product.

The ETF wrapper is not done expanding.

The next wave is already in the queue, and the firms that understand both the opportunity and the infrastructure required to support it will define what this industry looks like.

This article is intended for informational purposes only and does not constitute investment advice. It should not be relied upon as a recommendation, offer, or solicitation to buy or sell any security or adopt any investment strategy.