For years, the ETF industry operated on a simple truth: cut fees, win flows.

The race to zero defined a generation of product strategy, and index funds built on dirt-cheap beta became the dominant force in asset management. That playbook still works, but it no longer tells the whole story.

New data from Bloomberg Intelligence suggests the ETF investor base is broadening.

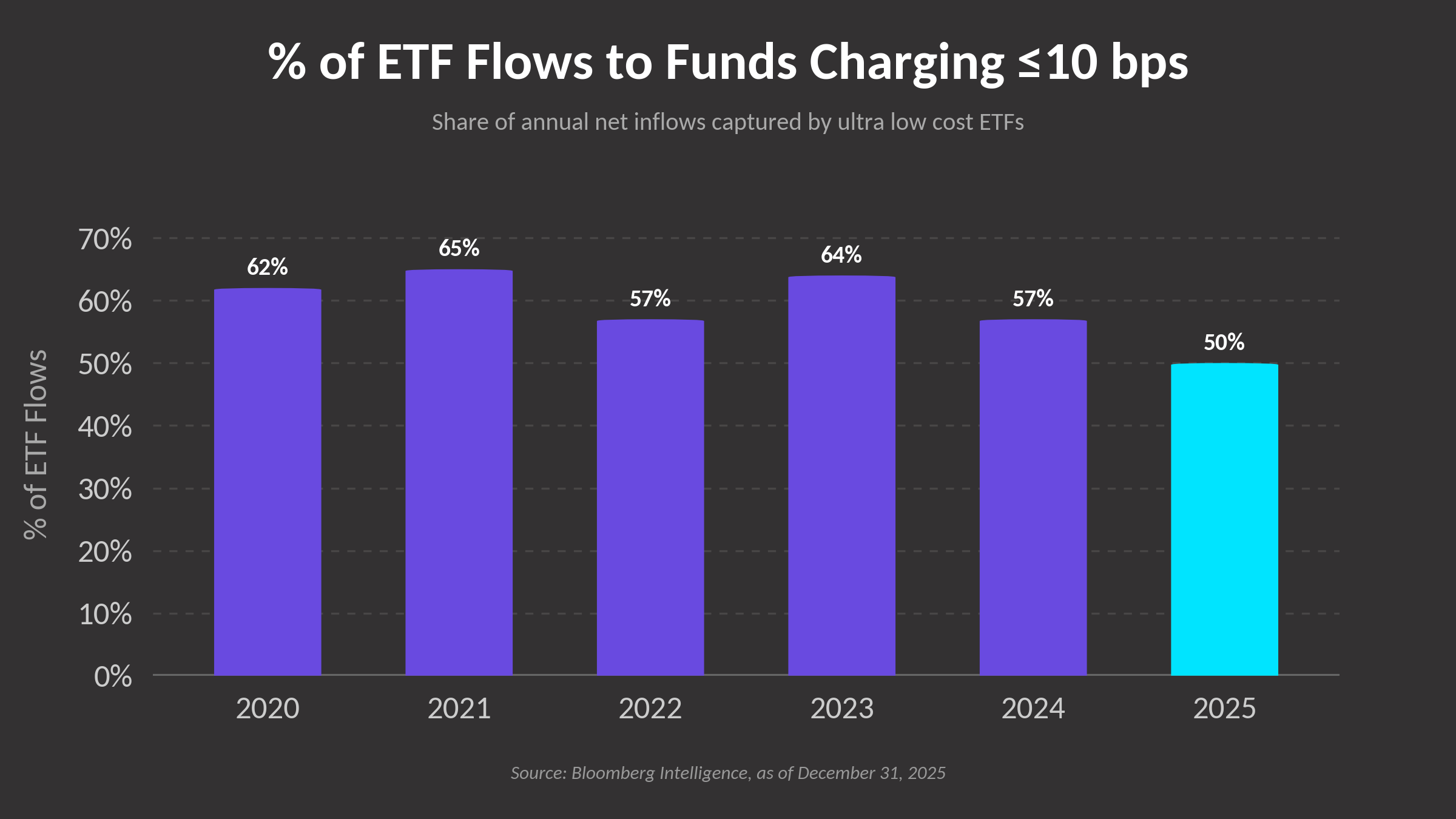

In 2025, only 50% of ETF flows went into funds charging 10 basis points or less, the lowest share in years and down sharply from roughly 65% in 2021 (see Chart 1). What is important to note is that investors are not abandoning low-cost products. Rather, the ETF tent itself has expanded, pulling in a new wave of strategies built around income generation, downside mitigation, and derivatives-based outcomes that are not typically available at the lowest fee tiers.

Chart 1

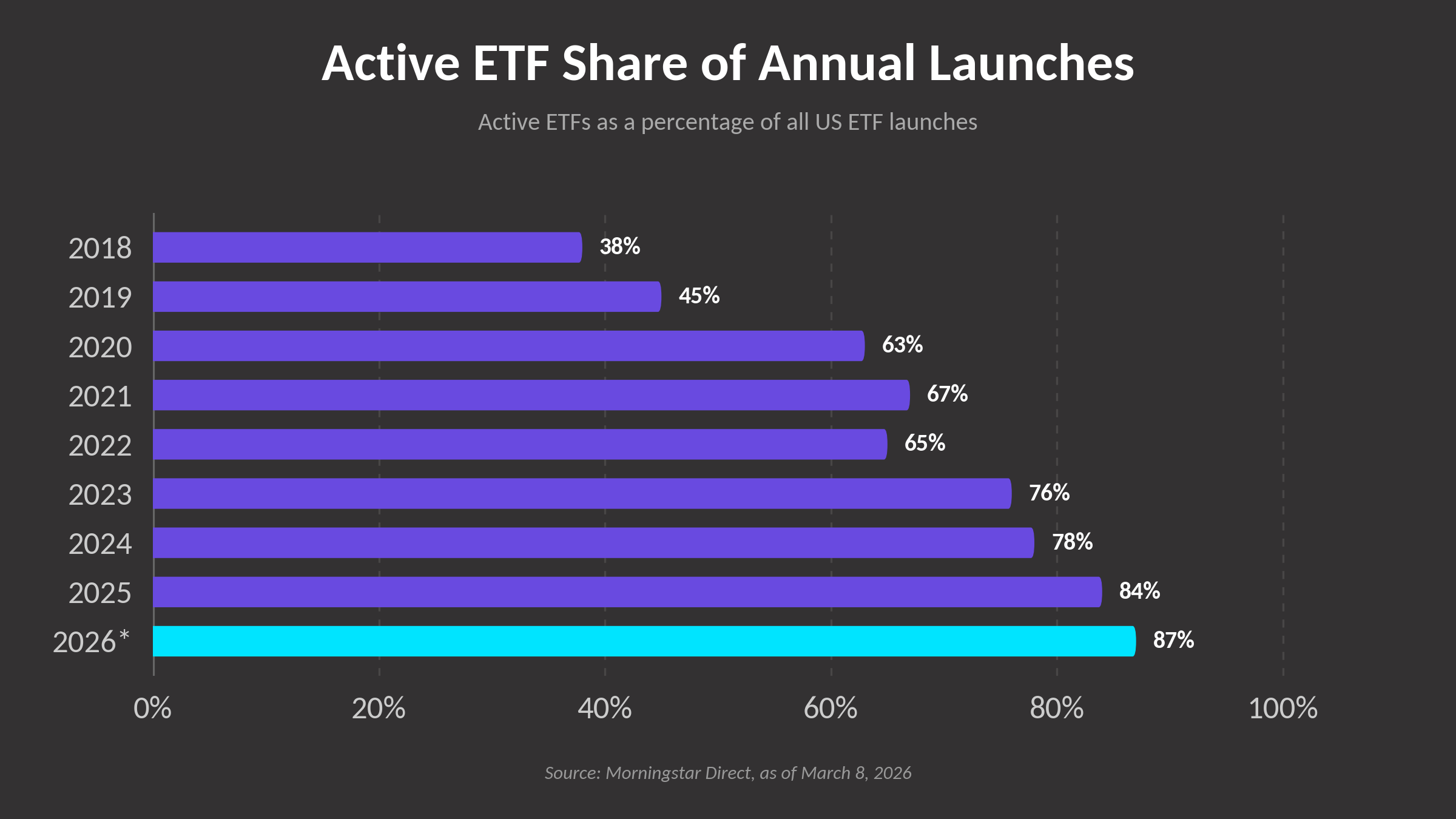

Active ETFs now represent 51% of all ETF products on the market, capture 33% of industry flows, and account for 26% of revenue, even though they represent just 10% of total AUM (Bloomberg Intelligence, as of October 31, 2025). Asset managers appear to be reading the same data. Active ETF launches have climbed from just 38% of all new issuance in 2018 to 87% so far in 2026 (see Chart 2). Last year alone, +890 active ETFs came to market versus only +170 passive launches (Morningstar Direct, as of December 31, 2025).

Chart 2

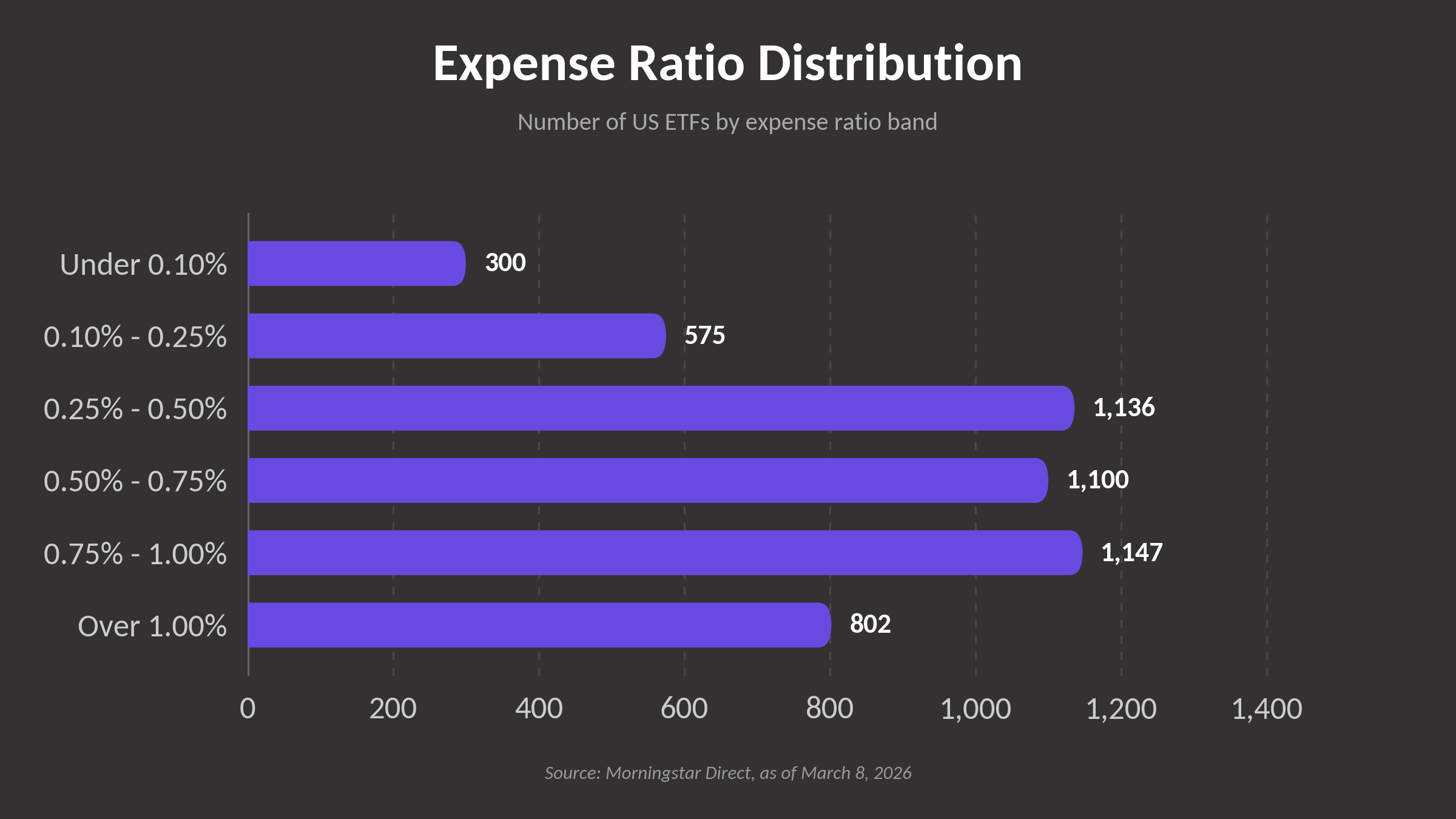

The product shelf reflects it too. Only about 6% of the roughly 5,000 ETFs on the market today charge under 0.10%. Nearly 45% sit between 0.50% and 1.00%, and another 16% charge more than that (see Chart 3). The data suggests investors are increasingly choosing strategies that cost something, and in growing numbers they appear comfortable doing so.

Chart 3

Many of the strategies driving those flows fall outside the traditional stock-picking model. Industry analysts have described the new wave of active as an evolution into buffer ETFs, covered call strategies, smart beta, and ETF model portfolios. Morningstar data points to a similar trend: the derivative-income category saw the most net inflows of any ETF category in 2025 (Morningstar Direct, as of December 31, 2025). BlackRock has projected that outcome-oriented ETFs, including covered call and buffer products, could reach $650 billion in assets by 2030 (BlackRock, as of June 2025).

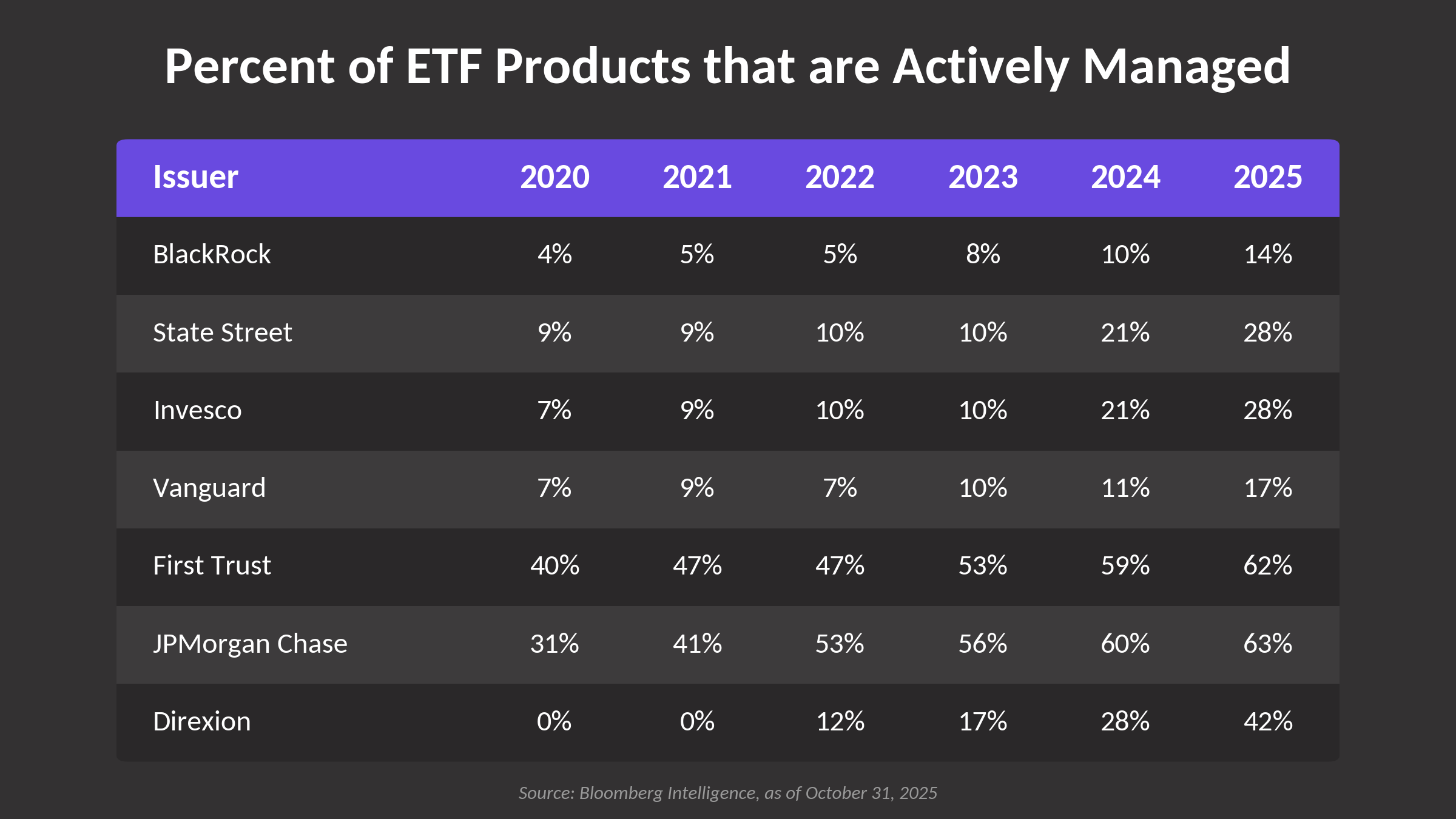

The largest issuers have not missed this signal.

JPMorgan Chase grew the active share of its ETF lineup from 31% in 2020 to 63% in 2025. State Street moved from 9% to 28% over the same period. Even Vanguard, the institution most associated with the low-cost passive movement, expanded its active ETF share from 7% to 17% (see Chart 4).

Chart 4

The scale of the broader migration adds context.

From 2019 through late 2024, investors moved more than $600 billion into active ETFs while pulling nearly $2 trillion out of active open-end mutual funds (Morningstar Direct, as of October 31, 2024). The ETF wrapper, with its tax efficiency, intraday liquidity, and lower costs relative to mutual funds, appears to be an increasingly common delivery vehicle for active and complex strategies. That dynamic pushed total U.S. ETF flows to a record ~$1.5 trillion in 2025, surpassing the prior year’s record by ~$350 billion (Morningstar Direct, as of December 31, 2025).

None of this means low-cost indexing is losing. The point is more nuanced: investors are no longer choosing between cheap beta and expensive active in the traditional sense. They are increasingly reaching for strategies that deliver specific outcomes, generate income in volatile markets, or provide structured protection, and appear willing to pay for that specificity inside the ETF wrapper.

For ETF issuers building and managing these complex strategies, the infrastructure required to execute them well has never mattered more. Tidal Financial Group’s large-scale derivatives risk management program and trading capabilities, built to support precisely these kinds of strategies, position it as a purpose-built platform for the next generation of ETF product development.